2026 Global Marine Lighting Market Forecast

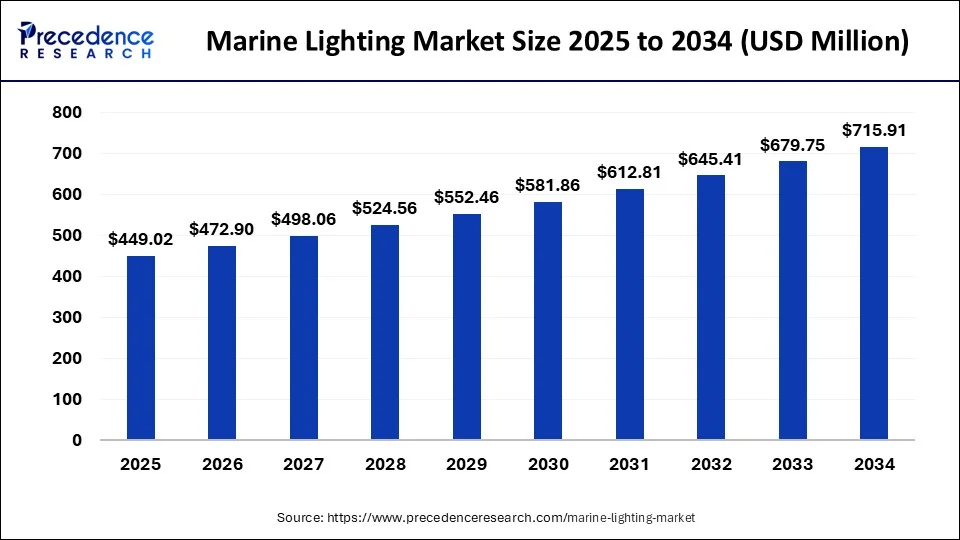

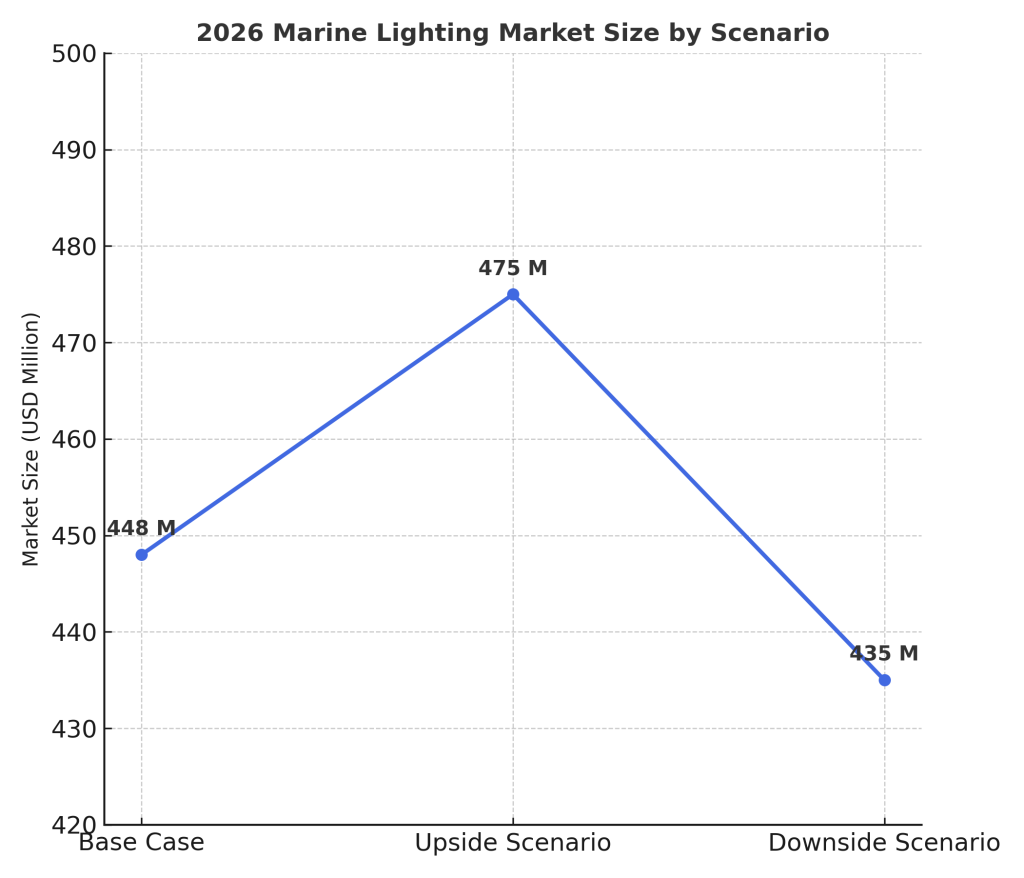

The state of the cruise industry, as shipbuilding cycles continue, recoveries, and as the International Maritime Organization (IMO) gets closer to finalizing regulations, along with investment in offshore engineering and wind power, the marine lighting market will be shaped. Considering the last available market data of the world’s public market research institutions, marine lighting will reach about USD 448 million in 2026 and with an average (CAGR) of roughly 2.5% it will continue into the years 2024-2026.

The scope of ship replacement. If the orders of shipbuilding accelerate and in synergy there overlaps with the replacement cycles, then the market value at the ETA 2026 will expand to the USD 470-480 million. Asia and the Pacific is the most dominant market and Europe and North America will continue their steady increase in value owing to the regulations, the cruise industry, and offshore engineering.

Table of Contents

Market Baseline and Growth Model

The global marine lighting market size in 2024 is USD 426.33 million according to Precedence Research. This figure demonstrates the pandemic-related recovery in ship deliveries in tandem with the structural modernization of LED marine lighting. Analyzing the cyclical nature of the shipbuilding industry, global energy transportation demand, renewed cruise industry activity, and the technological modernization of aging fleets, the market growth model for 2026 is anticipated with greater specificity.

Base Case

For the Base Case, the marine lighting market will likely grow to a 2.5% CAGR from 2024 to 2026. As newbuilds are delivered steadily, this market will be boosted. The shipyards that are forecasted to finish the large number of orders placed during 2022-2024 are the ones in China, South Korea, and Japan, and are concentrated on 2025-2026. With every new ship built, there are a large number of lighting units that will be needed, falling in a wide range of 150-400 lights needed per ship which will cover things such as the navigation lights, deck lights, cabin lights, engine room lighting, and emergency or signal lights. Newbuild construction will be the most reliable stable source of demand.

Each year, there are 100,000 commercial vessels in the world that have to do regular maintenace, and 8 to 12% of these enter a periodic maintenance inspection cycle, skipping vessels leaves the market. With no regulation changes, there will be a 5 to 8 year replacement cycle for LED lights. This leaves a large and consistent demand. In total, this gives a great base as a market for construction to work with.

There are no worries regarding International Maritime Organization (IMO) or clsassification societies in 2024-2026. There will be a neutral recovery regarding global trade that will result in expensive supply chain costs. These situations point towards a time , along with reasonable stablity, of moderate growth for the marine lighting industry. There will be expected project completion activity through global shipyards.

Upside Scenario

If all goes well, the global market for marine lighting should expand 5% to 5.9% every year from 2024 to 2026, and that’s due to the accelerated construction of ships in the Asia-Pacific area for the region. China, South Korea, and Japan dominate more than 92% of the market. Their shipyards, particularly in China and South Korea, are booked for the years 2025 and 2026. There are more and more orders for oil tankers, LNG carriers, and container ships. Shipyards are busier, more automated, and digitally constructed than ever, all of which will further heighten the industry’s shortage of marine lighting. More ship construction will have to be done and more marine lighting will be needed to meet the growing demand.

In addition, cruises are also expected to be operating at full capacity, which will also add to the demand for marine lighting. According to the latest estimates from the Cruise Lines International Association, the number of cruise passengers will recover to pre-pandemic levels by 2026. Each new cruise ship required lighting and high-end lighting equipment such as construction and decorative lighting, stage and high outdoor performance lighting. There is also a growing demand for lighting on cruise ship refurbishments. There is expected to be a steady increase in demand for high-end lighting, which in turn will increase the demand for marine lighting as well.

The growth curve will become even steeper with the new IMO regulations expected on the last quarter of 2026. If limitations become laws regarding energy efficiency in navigation lights visibility and intensity, EEXI/EEOI, emergency and LSA, explosion-proof LSA on oil and chemical carriers, and standardized green LSA, there will be a rapid replacement cycle over the aging fleet within 1-2 years, especially over vessels older than 10 years. When you add this regulatory surge to the newbuild deliveries and the recovering cruise industry, it is undoubtedly some of the biggest growth compounded. The 2026 marine lighting market is bound to go over the expected 470-480M.

Downside Scenario

In the worst-case scenario, the global marine lighting market is expected to show a modest CAGR of 0.5% from 2024–2026, given the risks associated with the macro economy and the industry cycle. A downturn in international economic activity, or a trade activity slowdown, would constrain market growth due to a reduction in major vessel orders like container and oil tanker ships, which in turn slow newbuild deliveries and limit market growth.

At the same time, marine lighting depends, critically, on the specific electronics and other materials like LED chips, aluminum and stainless steel, as well as power driver modules, and the optical lens materials. 10–25% increases in the prices of these other important inputs could cause a downward shift in market expansion as ship owners and shipyards defer procurement.

In addition, the market demand for high end, expensive, value lighting systems would suffer from any greater than expected cruise industry recovery delays. Given the scope, scale, and expense in cruise lighting systems, such a delay would mean the overall market growth would be low, or possibly in a down slope. This emphasizes the negatively down spiral of the industry, which is the main part of the worse case scenario.

Factors Driving the Growth of the Marine Lighting Market

Expected Growth of Deliveries of New Ships 2025 – 2026

There was a considerable increase in the global order of new builds in 2023 – 2024. This caused a spike in the delivery of new builds in 2025 – 2026. Each vessel installed has a complete. lighting system that contains navigation, deck work, engine room, accommodation, safety, and other specialized lighting. New build projects creates a considerable increase in the demand for specialized protective and smart systems. New builds of varied vessel types – container ships, tankers, LNG carriers, ro-ro vessels, and cruise ships – create a demand for various systems that increase the marine lighting market capacity.

How the Cruise Industry is Recovering Post Pandemic

The Cruise Lines International Association (CLIA) compiles shipping industry statistics, and they show that the number of international cruise passengers is increasing every month. It is expected that the cruise industry will have the same capacity as 2019 in the near future, this could be around 2026. When comparing a cruise vessel to a merchant vessel, cruise lines have significantly more required lighting fixtures. This includes broad architectural lighting, ambient and decorative lighting, functional task lighting, and emergency lifesaving lights. All of the projects that include new builds and refurbishments have lighting fixtures that will be in high demand, and that will increase the potential and the profitability of the range of products.

Expansion of Projects Offshore and of Offshore Wind

The investments are increasing in the three areas of the world – Europe, Asia-Pacific, and the Middle East – in the offshore oil and gas platforms, support and supply vessels for offshore, Wind turbine installation and Operations and Maintenance (O&M) ships. These vessels are in constant need of professional and commercial lighting designs, and in these delayed extreme sea environments, the need for operational protective high-grade (IP67-IP69k certifications) are in standard use. This is where the industry is moving in advanced and higher level specifications and higher value.

IMO Regulation Expectations Triggering Replacement Cycles

By the second half of 2026, the International Maritime Organization is likely to begin implementing or enforcing some core compulsory lighting standards for energy efficiency, safety, and environmental performance. This, in turn, will induce concentrated upgrade cycles for the navigation, signal and emergency lighting systems of older ships. Regulatory-driven replacement cycles are usually mandatory and concentrated, resulting in short-term market spikes and increased demand for the highly capable and smart lighting systems.

Accelerated Improvement of LED Technology

As LED technology becomes more advanced and more affordable, smart lighting with features like auto dimming, remote monitoring, and condition diagnostics has become common in new constructions and refurbishments. When paired with EN 60529 Grade IP67 through IP69K, shock resistant, and corrosion resistant designs, safety and reliability is greatly improved. The result is better vessel value and a global trend towards intelligent and high value marine lighting. This continues the long term demand for advanced LED solutions resulting in a sustainable growth in the market.

Factors Hindering the Marine Lighting Market

Supply Chain and Raw Material Price Volatility

The production of marine lighting relies on parramount elements that are the building blocks of the lights like LED chips, Driver ICs, optical lenses, and specialty metals. When the prices of the raw materials needed to make the components rise, the constructions budgets for shipboard equipment manufacturers get even tighter. This lead to a cycle of prolonged estimated time of arrivals (ETAs) for orders to be placed and delivered. These slow procurement processes can also lead to a drafting of new product specifications that only include a portion of the original product. There are also many other pressures that can be affected by the rise in prices such as shipping and other logistical components of the supply chain. There is a departure from the customary stable price of the market, leading to a loss in the overall structural value that certain specifications of the market provide. This mainly impacts the larger deployment targets as opposed to advertised targets.

Risks in Shipping Demand

As the economy slows, trade contracts or geopolitical tensions arise, the demand for ship transport decreases. Less volume in shipping translates to less demand in newbuilds and maintenance budgets. Vessel delivery times are extended and lighting systems are procured less frequently. Macro economics influence demand for lighting on container ships, oil tankers and bulk carriers. Therefore, prolonged periods of inactivity in the shipping industry create a lag on demand for ship lighting in commercial and specialized fleets.

Cruise Industry Recovery Below Expectations

The cruise industry is critical to the marine lighting market due to its specialized lighting systems. With consumer spending and tourism recovering at a slow pace, the new builds and refurbishments for cruise ships will likely be put on hold or scaled down. This will likely reduce the demand for embedded, functional and emergency lighting systems, as well as decrease the decorative lighting market value lower overall, thereby restraining the upper market growth.

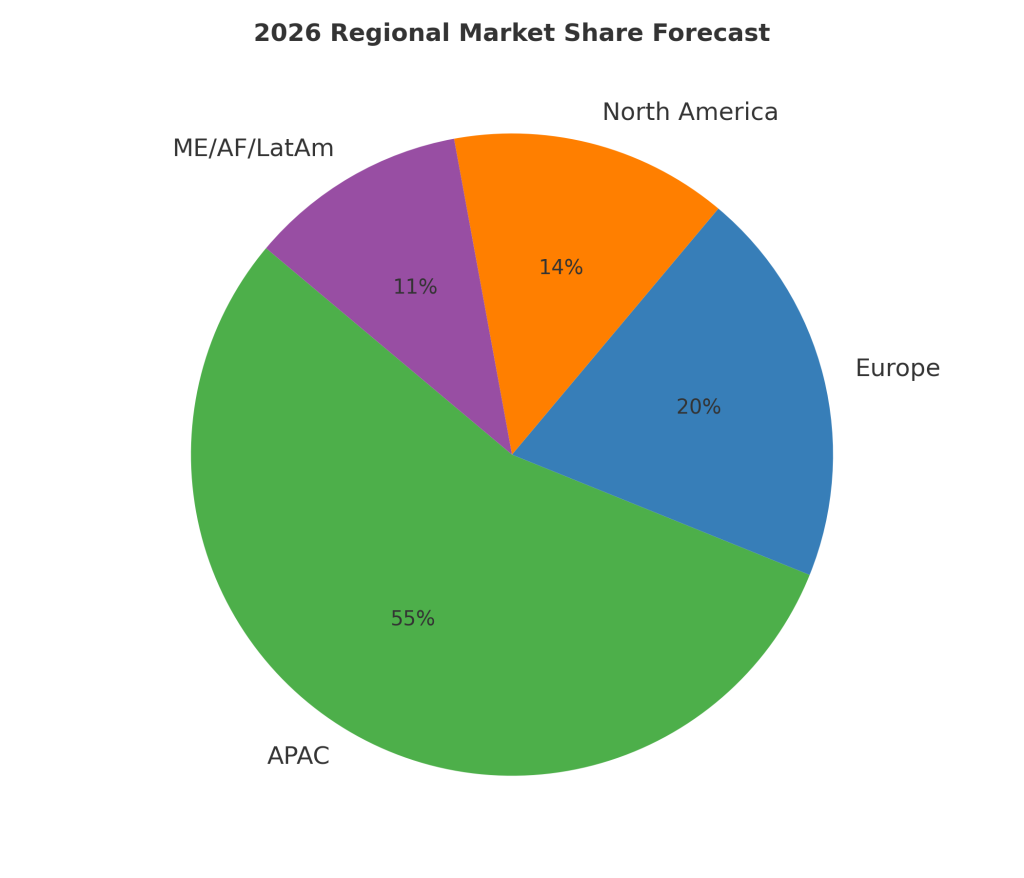

Regional Market Forecast for 2026

Based on publicly available reports and industry investment trends, the global market structure for marine lighting fixtures in 2026 is projected to be as follows:

| Region | Market Share | Forecast Size (USD M) | Regional Trend Analysis |

| Asia-Pacific (APAC) | 50%–60% | 224–269 | It accounts for more than 90% of all new construction with no close competitors. The peak new construction delivery period of 2025–2026 will greatly enhance the market. |

| Europe | 18%–22% | 80–99 | The concentration of cruise ships, offshore wind farms and other major projects creates a constant demand for mid to high end lighting. |

| North America | 12%–16% | 54–72 | The increase in luxury smart lighting is linked to commercial shipping vessels and yachts market growth. |

| Middle East / Africa / Latin America | 6%–10% | 27–45 | Uneven small-scale development in the market due to fluctuating investments due to fleet renewals in the energy and fisheries fields. |

Why is 2026 a Crucial Turning Point

Impact of New Delivered Ships and Fleet Changeovers

Many newbuild orders confirmed for 2024 and 2025 are expected to be delivered for the first time in 2025 and 2026. Also by then, the regulations, energy efficency requirements and safety compliance revisions with age of the vessels will compel replacement of their lighting systems and upgrade of their vessels. New + replacement will make 2026 a major, cycle-determining event for the marine lighting market having a dual effect of amplifying market scale and propelling the uptake of smart and more sophisticated lighting.

Vessels, Cruises, and Luxury Yates to Make a Full Recovery Soon

The segment of high-end leisure vessels and cruise ships is expected to recover to its pre-COVID market size and revenue by 2026. The market’s requirements and expectations diversify beyond the previous basic parameters of functionality to comfort and design and overall atmosphere. These trends undergo a shift from basic, low-cost, functional lighting to systems and designs that are considered high value and expensive, smart, and integrated. “Lighting investment per vessel increased sharply.”

The Increased Use of LED, Smart, and Sustainable Products

Many ship owners, shipyards, and operators are able to invest in better performance and lower maintenance LED lights because new smart LED tech is more affordable and efficient, and new smart LED features become available like dimming, remote control, condition monitoring, and smart monitoring systems. The new LED smart tech systems are also corrosion resistant, waterproof, and are shock resistant. The global marine market’s growth in high-performance and low maintenance lights is also in line with more sustainable and high end smart solutions sophistications.

Conclusion

Analyses of public market data and industry trends suggest the Marine Lighting Market will have slight growth with major developments within the industry due to developments within the technology used within the market. Top market players will make 448 Million and if the conditions are correct will earn around 470-480 Million. Most of the growth will come from the Asia-Pacific Region with Europe and North America having a sustaining effect. With the mass adoption of LED technology and smart systems with higher graded protective solutions, the product structure with the market will continue on the upward trend.